.svg)

The clients of the relocation industry will be impacted by escalating environmental concerns, societal expectations, and the undeniable reality of climate change. As a result, sustainability has become a critical component of global governance across all industries, including global mobility. The regulatory terrain of sustainability is a complex landscape which is shaped by many instruments – national laws, international treaties, industry standards, and corporate policies, all of them trying to foster a way to a more sustainable future.

There have been numbers of initiatives in the last decade established or gaining more widespread adoption addressing a wide range of sustainability issues. However, when it comes to enforcing accountability, this is where the policies and national governments come into play through legislation and regulatory bodies. So far, the EU has been global leader in sustainability regulation, introducing several major initiatives in the past five years. At the end of 2019 the European Commissions presented a strategy on how to move the EU economy to a more sustainable “climate neutral” economic model called the European Green Deal with its ultimate objective to reach the climate neutrality by 2050. (1)

But there has been much more going on in the EU. Sustainability reporting for the investment related purposes (SFDR) (2), legislative proposal concerning sustainable business practices across business operations and value chains (CSDDD) (3), Carbon Border Adjustment Mechanism (CBAM) addressing the price of carbon between local products and imported ones in specific sectors, just to mention few. The focus in the Mobility industry is now on the Corporate Sustainability Reporting Directive (CSRD) which entered into force in 2023 and was designed to enhance and standardize sustainability reporting among companies.

Starting from next year, the EU’s Corporate Sustainability Reporting Directive (CSRD) mandates larger EU based companies (which are not subject to the NFRD) with more than 250 workers, €50 million in turnover, or €25 million in assets to report on greenhouse gas emissions if two of the criteria are met. (4) The implementation is phased between this year (which is the first year the larger corporations shall already gather the data for the report submission) to 2029 depending on the company size and listing status. The subjected companies will have to report according to European Sustainability Reporting Standards (ESRS). (5) It is estimated 50,000 companies across the EU will be affected. And what about companies which are based outside of the EU? Even these companies are not exempt from the reporting if they meet certain criteria. And many of the multinational players in the global mobility industry will fall into the category to be classified and obliged to report.

So, when we move towards the focus of the reporting, the key is to provide reliable and comparable data on ESG sustainability topics from the area of environmental practices and performance, social aspects of the business relating to human and labor rights and governance, meaning how they integrate sustainability practices into their company structures and decision- making processes. Companies also must report on double materiality. This concept expands on the traditional understanding of materiality in financial reporting by incorporating another dimension – environmental and social materiality into it. So, the businesses shall not only report on how ESG issues affect their business performance but also vice versa, how their actions and activities impact the societal set up and environment. And in the relocation industry where it is all about the moving, the impact cannot be overseen. And even though it is still not clear how the potential sanctions for non-compliance will look like, they are expected to be significant and country dependent as each member state will be checking the CSRD compliance within their national legal framework. As per example of a German company reporting with the German version of CSRD, they might get fined up to 10mil EUR or 5% of their total yearly turnover if they will not comply. (6)

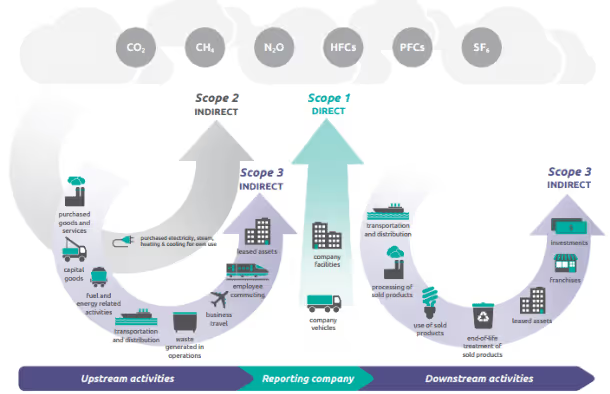

Greenhouse Gas Protocol and emissions reporting

When we zoom into the Environmental sustainability and reporting, a key variable to report on are emissions. Using the Greenhouse Gas Protocol (GHG) framework, companies are supposed to categorize greenhouse gas emissions occurring in the value chain into three scopes. Into Scope 1 which is addressing direct emissions, such as onsite energy usage, company-owned car fuel etc. Scope 2 includes indirect emissions resulting from purchased power, steam, heat, or cooling. Scope 3 is the trickiest one as it tackles emissions that extend beyond the reporting company’s limits and involve the whole supply chain. So, what is so tricky about the Scope 3 emissions?

They bring high complexity into the tracking process, particularly for businesses that track complex, extensive supply chains. Take the example of a car manufacturer, where vehicles comprise up to 30,000 components sourced from numerous suppliers. These suppliers’ activities influence emission data accuracy and transparency, which is crucial for comprehensive reporting. Similarly, managing Scope 3 emissions in the relocation industry involves coordinating with hundreds of suppliers, spanning real estate agencies, temporary housing providers, and moving companies.

“Value chain decarbonization remains a high priority. Nearly 90% of leaders report that Scope 3 reductions and net-zero targets are a top-three driver of their program.” (7)

To be able to report on emissions, measuring and tracking emissions is one of the first and most critical stages in helping any businesses understand the ecological effect of their activities. Because “You simply can’t manage what you don’t measure.” And without developing and a continuous refining of standardized processes and regulatory framework, it would be harder to maintain a balance between environmental protection, economic growth and social well-being, ensuring that sustainability is at the core of global governance.

Sources:

1. PWC

3. EU Lex

4. Sweep

6. PlanA

7. EcoVadis

Image credits:

1. Photo by Christian Lue on Unsplash

2. Photo by Gabriel Stanciu on Unsplash

3. Photo by by rawpixel.com on Freepik

3. GHG Illustration by GHG Protocol

.svg)